Core Concept 1: Scarcity and The Basic Economic Problem

25th August 2015

Scarcity and The Basic Economic Problem

Scarcity

The world’s resources are FINITE; there are only limited amounts of land, water, oil, food and other resources. Resources are therefore referred to by economists as being scarce.

Scarcity means that individuals, firms, governments and international agencies, known as economic agencies, can only obtain a limited amount of resources at any moment in time. For instance, families have to live within a budget and may not have everything need. A firm may wish to expand and not have the resources to do so, whilst the government may wish to build a new hospital or school but not have the resources to do so. Scarce resources are referred to as ECONOMIC GOODS.

Some resources are not scarce. Such resources are known as FREE GOODS, and might include air, for example. As resources have to be spent to preserve something then it no longer exists as a free good. For example, as pollution increases and causes greater resources to be spent on the purification of air it no longer exists as a free good but an economic good. Water was a free good, but as pollution has increased, it has become an economic good as a result of the money spent cleaning water sources, rivers and the sea.

Infinite Wants

People have a certain number of needs which must be satisfied in order for survival. Some of these, are material needs, such as food, liquid, heat, shelter, and clothing. Others are emotional such as love and friendship. People’s needs are finite, yet no one will decide to live at the minimum level of basic human needs if they can enjoy a higher standard of living. All human beings will want more of something, in other words human wants are unlimited. This might include a bigger house, a longer holiday, a cleaner environment, more love, more friendship, or more leisure time.

The Basic Economic Problem

Resources are scarce but wants are infinite. It is this which gives rise to the BASIC ECONOMIC PROBLEM, and which forces economic agents to make choices. They have to allocate their scarce resources between competing uses.

ECONOMICS is the study of this allocation of resources, – the allocation of these scarce resources by economic agent. Every CHOICE involves a range of alternatives. Governments and individuals face making choices daily. For example should they spend £1 billion on a nuclear bomber or build 6 hospitals. An individual might decide to spend £300 on a season ticket to Man Utd or buy 100 pack of cigarettes, or for instance have to choose between becoming an accountant, teacher or policeman.

These alternatives can be measured in terms of the benefit to be gained from each alternative. One choice will be the ‘best’ one and a rational person or government will choose that one. However as a result all other alternatives will have to be foregone. The benefit lost from the next best alternative foregone is the OPPORTUNITY COST. So if you had £300 and spent it on a Man Utd season ticket, then the opportunity cost might be the benefit lost from the 100 packets of cigarettes you could have bought.

Free goods have no opportunity cost, because no resources need to be sacrificed when someone breathes the air.

What is an economy?

Economic resources are scarce, but human’s wants are infinite. An economy is a system which attempts to solve this problem. There are many levels and types of economy.

Different levels of economy

The different types of economy are:

|

Free Market – Minimal government intervention

|

|

| Types of Economy |

Planned Economy – Gov’t makes resource allocation decisions

|

|

Mixed Economy – Features characteristics of both capitalism and socialism. |

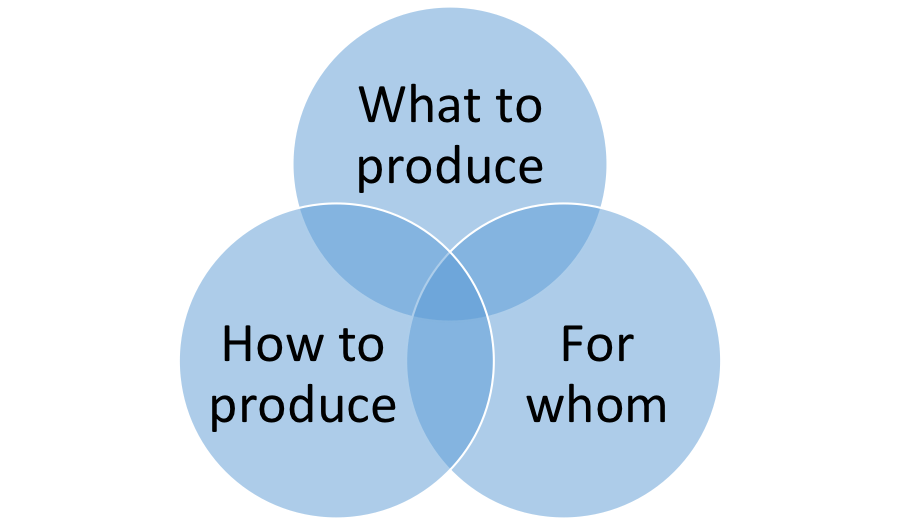

The Economic Problem

There are three parts to the economic problem.

What is to be produced ?

An economy can choose the mix of goods to be produced – For instance what proportion of total output should be spent on defence? What proportion of output should be spent on education? What proportion should be invested for the future? What proportion of output should be spent on manufactured goods and what proportion on services.

How is production to be organised ?

For instance, should compact discs be made in the UK, Thailand or Japan? How should a car be manufactured, using plastic or steel, using an automated assembly line or unskilled labour?

For whom is the production to take place ?

What proportion of output goes to workers and pensioners? What should be the balance between incomes in the UK and Bangladesh? In other words how are the goods produced to be divided?

Economic Resources

There are 4 factors of production; resources which are used in the production process. These are:

Land

This includes the raw materials below the earth, on the earth, in the sea and atmosphere. This might include everything from gold to rainwater and trees.

Non-renewable resources are these which once used are not replaceable. This would include oil, gas and coal. There use is finite.

Renewable resources can be used and are replaceable. For example fish stocks or trees. These are infinite in their availability. However in practice they may be over exploited which results in their destruction.

Labour

This is the workforce of the economy. This includes everyone who is working and those unemployed. Each production process requires some labour. Labour can be added to the process, or improved through training. Expenditure on education and training for labour is known as Human Capital investment. Thus the value of an individual worker is their human capital.

Capital

Capital is the manufactured stock of tools, machines, factories, offices, roads and other resources which are used in the production of goods and services. There are two types of capital : WORKING and FIXED CAPITAL. Working (circulating) Capital is represented by stocks of raw materials, semi-manufactured and finished goods which are waiting to be sold. These stocks circulate through the production process until they are finally sold to a consumer.

Fixed capital is the stock of factories, offices, plant and machinery. Fixed capital is fixed in the sense that it will be not be transferred into a final product as working capital would. The role of fixed capital is to transform working capital into finished products.

Entrepreneurship

Entrepreneurs are individuals who organise production, in other words land labour and capital in the production of goods and services. They will also take risks with their own money and the financial capital of others, they buy factors of production to produce goods and services in the hope that they might be able to make a profit, but in the knowledge that they could lose their investment and go bust. It is this element of risk undertaken by the entrepreneur which distinguishes him from the ordinary worker (Labour).

0 Comments