Increase in tax rates can reduce tax revenue

22nd February 2017

It’s one of the paradoxes of taxation that an increase in tax rates can lead to a fall in tax revenue.

For example, George Osbourne announced a higher stamp duty on properties over £1.5m in April of last year (2016), who would pay an extra £18.750 in duty – an overall level of £93,750 on a £1.5m home. They now pay 12% on the transaction value over £1.5m (the lowest rate is 2% for houses worth from £125,000 to £250,000. Below £125,000 there is no tax. For an example see below).

But the overall tax take from stamp duty fell from just over £1 billion in 2015 to £635m last year (2016).

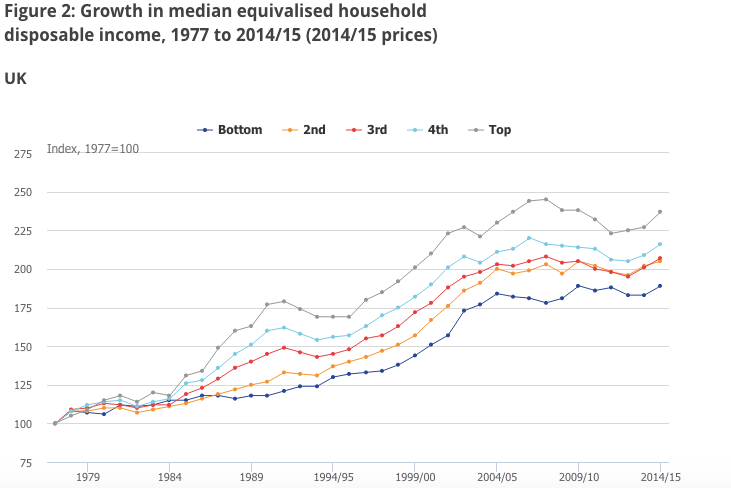

Since 1977, the average proportion of income households pay in direct taxes has generally fallen, most recently going from 21.4% of gross income in 2007/08 to 18.8% in 2014/15.

Income changes by each 20% quintile of the Uk working population – source National Statistics

Yet the graph shows that disposable income, after tax and benefits, for the lowest income 20% rose by 4% between 2007 and 2015 – due to the rise in the tax free income threshold to just over £10,000 last year and the change in benefits.

But for the top 20% disposable income fell by 5%. A higher rate of income tax was introduced on the 1% who earn over £150,000 (a rate of 45% introduced in 2013 to replace the old 50% rate) – but the tax take from this section of taxpayers actually fell that year – by £9bn. They still contribute 30% of the £290bn raised by income tax in the UK – but it may not be wise to over-tax them.

For a rise in tax rates can lead to a fall in tax revenue.

Example of how stamp duty is levied:

If you buy a house for £275,000, the Stamp Duty you owe is calculated as follows:

- 0% on the first £125,000 = £0

- 2% on the next £125,000 = £2,500

- 5% on the final £25,000 = £1,250

- Total SDLT = £3,750

0 Comments