Handout: The Meaning of Oligopoly

12th September 2015

The Meaning of Oligopoly

Oligopoly, which is sometimes called `imperfect competition amongst the few’, exists when there are just a few firms in the market (or just a few dominant firms). However, oligopoly is best defined by market conduct, or the behaviour of the firms within the market, rather than by the precise number of firms in the market and the degree of market concentration. For example, the effect upon profits of a price change undertaken by an oligopolist depends upon the likely reactions of the other firms; so when deciding a price strategy, an oligopolist must make some assumptions about the likely response of the other firms. Oligopoly is characterised by reactive market behaviour and by interdependence between firms, rather than by the independent choice of price or output which is assumed to exist in the other market structures.

Perfect and imperfect oligopoly

Perfect oligopoly is said to exist when the oligopolists produce a uniform or homogeneous product, such as petrol. By contrast, an imperfect oligopoly exists when the products produced by the oligopoly are by their nature differentiated, for example automobiles.

Competitive and collusive oligopoly

Competitive oligopoly exists when the rival firms are interdependent in the sense that they must take account of the reactions of one another when forming a market strategy, but independent in the sense that they decide the market strategy without co-operation or collusion. The existence of uncertainty is a characteristic of competitive oligopoly; a firm can never be completely certain of how rivals will react to its marketing strategy. If the firm raises its price, will the rivals follow suit or will they hold their prices steady in the hope of gaining sales and market share? Uncertainty can be reduced and perhaps eliminated by the rivals co-operating or colluding to fix prices or output in a cartel agreement, or even by allocating customers to particular members of the oligopoly.

Price competition and other forms of competition

When firms collectively agree to fix the market in conditions of collusive oligopoly, prices are of course likely to be stable. Evidence also suggests that prices are very often relatively stable in competitive oligopoly as well as when the firms can collude or co-operate with each other. Even though no formal – or even informal – collective pricing agreement exists, firms realise that a price war will be self-defeating for all the firms involved. They therefore may reach a tacit understanding not to indulge in aggressive price competition as a means of gaining extra profits or market share at the expense of each other. In the absence of keen price competition, oligopolistic firms are likely to undertake forms of non-price competition, such as: marketing competition, including obtaining `exclusive outlets’ such as tied petrol stations through which oil companies can sell their products; the use of persuasive advertising, product-differentiation, brand imaging and packaging; quality competition, including the provision of after-sale service.

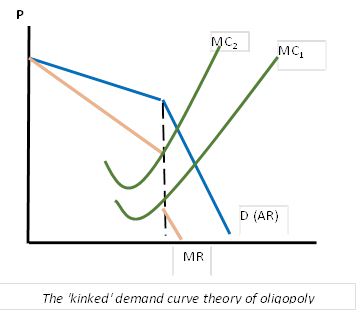

The kinked demand curve theory of oligopoly

This theory was originally developed to explain alleged price rigidity and the absence of price wars in oligopolistic markets. Assume an oligopolist produces the output Q1 illustrated in the diagram opposite, selling his output at price P1. The demand curve DD has been drawn on the assumption that the firm expects that demand for its product will be relatively elastic in response to a price rise because rivals are expected to react by keeping their prices stable in the hope of gaining profits and market share. Conversely, the oligopolist expects his rivals to react to a price cut by decreasing their prices by an equivalent amount; he therefore expects demand to be relatively inelastic in response to a decision to reduce price, since he cannot hope to lure many customers away from his rivals. The oligopolist therefore expects his rivals to react asymmetrically when price is raised compared to when price is lowered. As a result, he believes his initial price and output at point A to be at the junction of two demand curves of different elasticity, each reflecting a different assumption about how rivals are expected to react to a change in price. The oligopolist expects that profits may be lost whether the price is raised or cut. On these assumptions, the best policy is to leave price unchanged, resulting in sticky prices!

There is a further reason why prices may tend to be stable in conditions of `kinked’ demand. A mathematical discontinuity exists along a vertical line above output Q1, between the marginal revenue curves associated respectively with the relatively elastic and relatively inelastic demand (or average revenue) curves. The marginal cost curve can rise or fall within the range of this discontinuity, without altering the profit-maximising output Q1 or price P1. If marginal costs rise above MC1 or fall below MC2, the profit maximising output changes and the oligopolist must set a different price to maximise profits, assuming of course that the curve DD accurately represents the correct demand curve facing the firm. But the oligopolist’s selling price remains stable as long as the marginal cost curve lies between MC1 and MC2.

Activity: Other aspects of oligopoly pricing

Fit the appropriate term to the correct definition from the following list:

Barrier to entry, Limit pricing, covert collusion, Price Leadership, Price parallelism, Predatory pricing, Cost plus pricing, Price discrimination

…………………………… – simply means that a firm sets its selling price by adding a standard percentage profit margin to average or unit costs.

………………………….. – occurs when there are identical prices and price movements within an industry or market. It is worth noting that ………………………. can be caused by two completely opposite sets of circumstances. On the one hand, price parallelism would occur in a very competitive market, approximating to perfect competition, as the firms adjusted to a ruling market price determined by demand and supply in the market as a whole. But on the other hand, ………………………….. results from price leadership in tightly oligopolistic industries.

………………………….. – Because overt collusive agreements to fix the market price, such as cartel agreements, are usually made illegal by government, oligopolistic firms use less formal or tacit ways to co-ordinate their pricing decisions.

An example of ………………………….. is price leadership, which occurs when one firm becomes the market leader and other firms in the industry follow its pricing example.

………………………….. – The central assumption of the `…………………………’ theory is that established firms in the market set their prices taking into account the effect they may have on long-run profitability by possibly attracting new firms into the industry who would erode their monopoly power. Firms may decide to set prices which, by deterring the entry of new firms, act as a …………………………… Thus the established firms sacrifice the short-term maximised profits which higher prices would yield in order to maximise long-run profits, achieved through preventing or limiting the entry of new firms.

………………………….. – Whereas limit pricing deters market entry, successful ……………………………. removes recent entrants to the market. ………………………….. occurs when an established firm deliberately sets prices below costs to force new market entrants out of business. Once the new entrants have left the market, the established firm will usually restore prices to their previous level.

………………………….. – occurs when firms charge different prices to different customers based on differences m the customers’ ability and willingness to pay. Those customers who are prepared to pay more are charged a higher price than those who are only willing to pay a lower price. It is important to note that the different prices charged are not based on any differences in costs of production or supply.

0 Comments